by John Titus

Despite being over a century old (and indeed having been written in 1912–one year before the Federal Reserve Act became law), U.S. Money vs. Corporation Currency by Alfred Owen Crozier is easily my favorite book about the Fed, as much for its plain-spoken and logical approach to issues as for the author’s insights as a passionate participant in the events he’s describing.

|

Crozier describes the machinations of Wall Street banks against Main Street in plain language that reveals how the passage of the Federal Reserve (then called the National Reserve Association) Act would only increase Wall Street’s control over the country. I’ve gone back to the book any number of times for the author’s take on certain monetary points, so reliable is Crozier’s grasp of the plumbing that underlies much of American finance. |

|

In retrospect, it doesn’t surprise me that I had difficulty even obtaining the book (though I now see it available on amazon), finally tracking it down on bookfinder.com. Notably, lesser though more sensational books are not only widely available but endlessly hyped.

“U.S. Money” refers to money issued by the U.S. Treasury pursuant to the constitution. “Corporation Currency,” by contrast, refers to the proposed issuance of credit (really, credit-money) by a single private bank, namely, the Fed. That distinction–ultimately legal in nature–is absolutely essential to Wall Street’s looting operation against Main Street, as the book explains. Crozier goes through example after example of how the basic U.S. monetary structure (which was intact long before the Fed was created) had been working deep and unjust extractions on Main Street for several decades before Wall Street bankers sought to at once streamline and enhance their advantages by way of central bank legislation.

In this connection, Crozier does a very good job of describing what a fair and just (and legal) monetary system looks like in the first place, using historical examples of honest and effective money, so that readers can more easily see by contrast how credit-money is used as a weapon by Wall Street against Main Street.

Crozier was a lawyer by training but avoided legalese in favor of straightforward language using practical examples. Crozier’s logic, razor sharp as it was, is helped by his easy writing style. He used these gifts to expose the sharp tactics and rip-offs used by the extremely wealthy against ordinary people, all of which make the author an extremely dangerous enemy of the Federal Reserve. And while the Fed has certainly had many of those since Crozier wrote, I see in in him three crucial traits that distinguish him over every one of his successors:

-

(1) Crozier understood that Wall Street’s long history of successes in artificially triggering financial panics (to enrich itself at Main Street’s expense) hinged on the inherent vulnerability of credit-money (“corporation currency”) to violent and sudden contraction–a weakness not found in real, legal tender money (“U.S. Money”); this distinction is lost entirely, curiously enough, on both right-leaning critics complaining of “fiat money” at every opportunity and left-leaning MMT proponents, who wrongly insist that all money is debt;

(2) Crozier understood and freely wrote about the fact that Wall Street banks perpetrated crimes every day in their ordinary course of business, and that the then-pending Federal Reserve Act would only strengthen those same criminal banks by concentrating their power; monetary writers since Crozier have largely danced around the subject of crime if they acknowledge it all; and

(3) Crozier traveled in the same circles–professional as well as social, one may surmise–as many prominent Wall Street figures and high-ranking political figures, including U.S. President Howard Taft, so the author knew first hand about the sociopathic and often criminal class of people he was writing about.

|

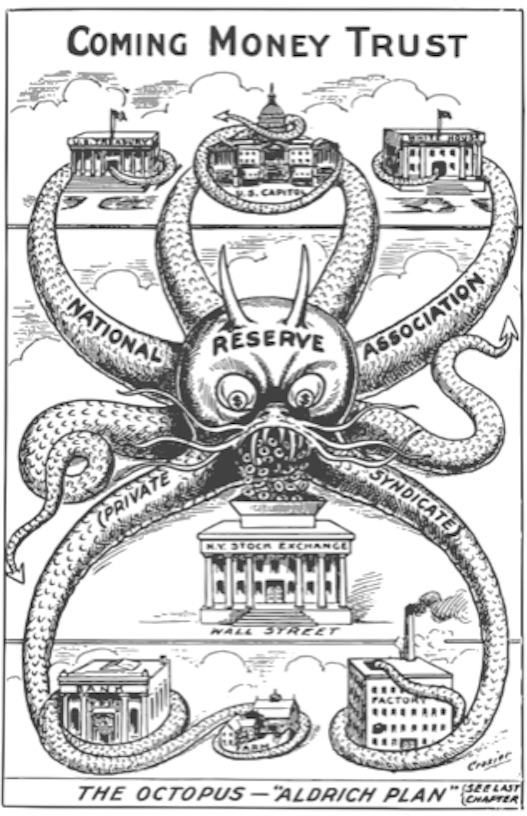

As formidable as those traits are by themselves, it’s ultimately Crozier’s sheer passion for his subject that makes him such a joy to read. His passion is palpable from the opening pages of the book, which includes a now-famous illustration of a monstrous Wall Street Octopus, labeled “National Reserve Association” (the draft name of the Fed) strangling several venerable American social institutions with its tentacles–an illustration done by… the author himself. |

|

“The Octopus” is just the first of 34 illustrations penned by Crozier’s own hand specifically for the book. Crozier was nothing if not resourceful, and he used whatever tool he needed carry out his fight against centralized graft and corruption of the monetary powers of his day.

Along these same lines, Crozier includes in the book some 30 letters that he exchanged with a variety of Wall Street institutions and politicians on the topic of the “National Reserve Association,” as it was then called. Again and again Crozier would lure his banker-correspondents into debates on monetary points with questions that the bankers evidently interpreted as ignorance, only to find themselves checkmated one or two letters hence, at which point they would punt on the discussion in amusing ways.

In this latter pursuit, Crozier can be accurately seen as an actor in the very story that he was telling, and his forthrightness about his views on matters is refreshing: Crozier was dead set against the passage of the central bank legislation he was writing about, and did a magnificent job of explaining why that was so. In a very real sense, Crozier wasn’t just an author–he was an activist as well, and a very effective and persuasive one at that. But Crozier’s activism doesn’t really fit the mold that emerged over the subsequent century: rather than leading the charge among people on the street, Crozier carried his fight to his enemies on their own turf. The record he left behind is invaluable for that reason alone.

As well, Crozier traveled where needed in opposition to the pending Fed legislation. Indeed the book is peppered with scenes in which Crozier himself makes an appearance, even meeting with President Taft. See Appendix, p. 358 (“On November 16, 1911, the author of this volume met with President William H. Taft in the White House at Washington to discuss certain proposed changes in the monetary and banking laws and particularly the so-called ‘Aldrich Plan’ for a private central bank urged by the National Monetary Commission.”)

Crozier was invested in his story in another important sense as well: it appears that he self-financed the book’s publication, possibly using proceeds from his critically acclaimed Wall Street romance novel from 1906, The Magnet. Whatever the case, it appears that not much has changed in the publishing world, which for my money has yet to produce a single work that rivals Crozier’s for both precision and clarity concerning the dangers of the Fed.

Provided below are a few excerpts from the book that offer Crozier’s insight on various topics:

• On how a contraction of the money supply is good for Wall Street banks (p. 101):

-

Any serious reduction in the supply of money or credit, or increase in the interest rate, creates conditions that immediately begin to lower the general wages paid labor and lengthen the hours of work. It also demoralizes the price of all property and all securities, except bonds bearing a fixed interest rate, by reducing dividends. Mortgages and bonds bearing fixed interest rate are increased in value by contracting the supply of money because the fixed income will buy more property and labor at lower prices. The bulk of the vast bond or fixed income wealth of the world is owned by the banks and by other incorporated and individual holders here and abroad.

• On how banks and their customers can be controlled by outside forces, particularly a large centralized force like the Fed (p. 363):

-

When the banks are fully loaned up, if by withdrawals or otherwise their cash reserves are decreased half, under the law they must decrease their total loans one-half. They must force their customers suddenly to pay up loans aggregating eight to twelve times the shrinkage of cash reserves. If a half billion is thus withdrawn from bank reserves business borrowers must pay up at once over five billion dollars of loans due to the banks (an amount more than twice the total of all money in circulation in the United States), no matter what sacrifices of securities, properties and commodities it entails. The banks cannot do other than force such payments even if it closes industries, plunges labor into idleness, causes general distress, panic and financial ruin.

-

A private corporation with power suddenly to contract the outstanding public currency without limit, of course thereby could almost to any extent deplete the reserves of the banks and force them immediately to call in their loans in such volumes that general panic and financial disaster would be inevitable. Likewise by inflating the currency it could increase bank reserves and enormously and even dangerously expand the loaning power and profits of the banks.

• On Wall Street’s criminal business model (p. 192):

-

It is common knowledge that big Wall Street banks daily ignore and break both the spirit and plain letter of the National Banking Law, illegally loaning sums aggregating untold millions to further stock market operations of the Wall Street masters of such banks. ‘High finance’ knows no law, human or divine. It is a bold and daring outlaw on the highway of commerce, making frequent raids to ‘hold up’ honest business and plunder American prosperity.

• On the real point of the Federal Reserve Act (then “the Aldrich plan”)(p. 101):

-

The Aldrich plan would put the ownership, control and management of the National Reserve Association, with power to inflate and contract the quantity of money without limit, in the hands of the very private interests that would most profit by an abuse of that dangerous power. And every dollar gained by those interests through excessive inflation and contraction of the volume of currency would come out of the pockets of the people of the United States.

• On how the proposed central bank legislation relates to America’s history of bank panics (pp. 263, 274):

-

It is American history, the fact that every great panic has immediately preceded a very great joint effort by Wall Street and the big banks to put through Congress legislation vastly increasing the profits and power of the banks and Wall Street.

- * * * *

-

The Aldrich plan seeks only to protect banks, to make banks panic-proof. It does not make the country proof against panics. In fact it grants to the National Reserve Association power to cause panic any time by contracting the currency, which in turn instantly forces contraction of bank credit, or loans, ten times as much.

• Another example of Crozier’s activism (p. 194):

-

In 1908 writer suggested to the General Assembly of New York a legislative investigation of Wall Street and drafted a bill introduced for that purpose. He urged the plan at a public hearing in Albany at which John G. Milburn as counsel for the [New York] Stock Exchange publicly consented to such investigation. Evidently he was not serious, because agents of Wall Street blocked the measure notwithstanding Gove Hughes twice urged its passage in special messages.

I would urge Solari subscribers to get a copy or two of this excellent piece of history. If nothing else it will frustrate the efforts of google and company to erase our past.

Purchase U. S. Money vs. Corporation Currency Aldrich Plan HERE